Home Insurance Deductibles Explained: Everything You Need to Know

The deductible is one of the most misunderstood parts of a home insurance policy. It is simply the amount of money you agree to pay out of your own pocket before your insurance company pays a dime.

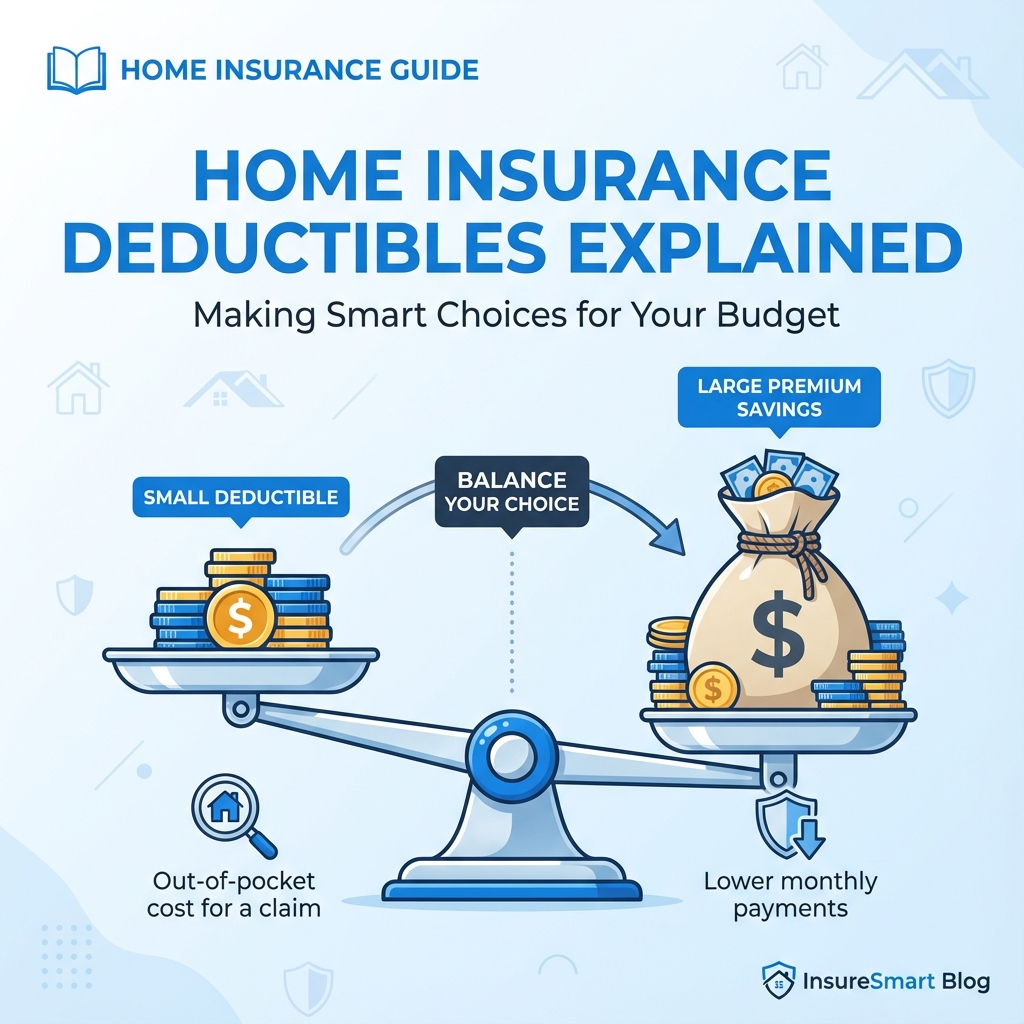

Choosing the right deductible is a balancing act. Choose one too low, and your monthly premiums will soar. Choose one too high, and you might not be able to afford repairs when disaster strikes. Here is how to find the sweet spot.

1. Flat Dollar Amount Deductibles

This is the simplest type. You choose a specific dollar amount, such as $500, $1,000, or $2,500.

How it works:

If a storm causes $5,000 in damage to your roof and your deductible is $1,000:

You pay: $1,000

Insurer pays: $4,000

2. Percentage Deductibles (The Tricky Part)

In many states prone to severe weather (like hurricanes or hail), insurers require a separate deductible for wind/hail damage that is calculated as a percentage of your dwelling coverage (Coverage A).

Common percentages are 1%, 2%, or even 5%.

Example Calculation:

Home Coverage Value: $400,000

Wind/Hail Deductible: 2%

Your deductible amount = $400,000 × 0.02 = $8,000

Warning: Many homeowners don't realize they have a $8,000 deductible until they try to file a roof claim. Check your "Declarations Page" carefully.

3. Split Deductibles

Your policy likely has different deductibles for different perils.

- All Other Perils (AOP): Usually a flat fee (e.g., $1,000). Covers fire, theft, liability, water damage.

- Wind/Hail: Often a percentage (e.g., 1%). Covers tornadoes and storms.

- Hurricane: A specific deductible triggered only by named storms (common in FL, TX).

When Do You Pay It?

You typically do not write a check to your insurance company. Instead, the deductible is subtracted from your claim payout.

If the repair costs $10,000 and your deductible is $1,000, the insurer sends you a check for $9,000. You are responsible for paying the full $10,000 to your contractor, using the $9,000 form insurance plus $1,000 of your own money.

Deductible Waiver

Some premium policies include a "Large Loss Waiver." This means if your loss exceeds a certain amount (like $50,000), the insurance company waives your deductible entirely. This is a nice perk, but usually costs extra.

Frequently Asked Questions

Can I change my deductible to save money? expand_more

Does liability coverage have a deductible? expand_more

HomeInsuranceQuotes360 Team

Policy Guides