Average Home Insurance Cost by State (2025 Breakdown)

Location, location, location. In real estate, it determines the value of your home. In insurance, it determines the price of protecting it. As we settle into 2025, the disparity between home insurance premiums across state lines has never been more pronounced. A homeowner in Vermont might pay less than $800 a year, while someone with a similar home in coastal Florida could see quotes upwards of $6,000.

Why such a dramatic difference? It boils down to risk. Insurers are in the business of predicting the future, and in some states, the future looks much stormier—and more expensive—than in others. In this comprehensive guide, we have compiled the latest 2025 data to provide you with a detailed state-by-state breakdown of average home insurance costs. We will also explore the underlying factors driving these rates and what you can do if you live in a "high-risk" state.

The Most and Least Expensive States for Home Insurance

Before diving into the full 50-state list, let's look at the extremes. Understanding which states sit at the top and bottom of the pricing spectrum helps illustrate the impact of regional risks.

trending_up Top 5 Most Expensive

- Florida: $6,000+ (Hurricanes)

- Louisiana: $5,300+ (Hurricanes/Flooding)

- Oklahoma: $4,800+ (Tornadoes/Hail)

- Texas: $4,100+ (Storms/Hail)

- Nebraska: $3,900+ (Severe Weather)

trending_down Top 5 Least Expensive

- Vermont: ~$700 (Low Risk)

- Delaware: ~$780 (Moderate Weather)

- Pennsylvania: ~$840 (Stable Climate)

- New Hampshire: ~$850 (Low Risk)

- Utah: ~$880 (Newer Construction)

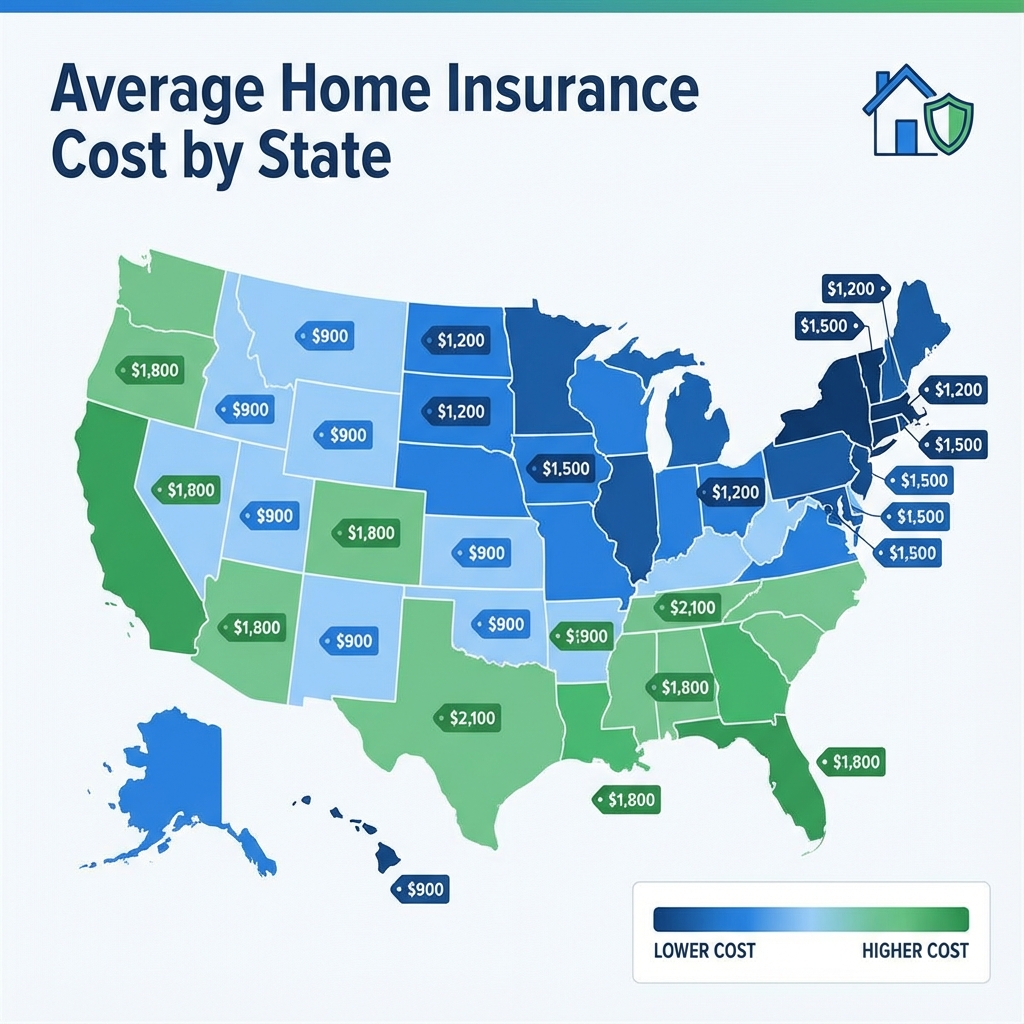

State-by-State Insurance Cost Table (2025)

The following table provides estimated average annual premiums for a policy with $300,000 in dwelling coverage. Keep in mind these are averages; your specific rate will depend on your home's age, your credit score, and your claims history.

| State | Avg. Annual Premium | Avg. Monthly Cost | Primary Risk Factor |

|---|---|---|---|

| Alabama | $2,900 | $242 | Hurricanes/Tornadoes |

| Alaska | $1,200 | $100 | Earthquakes/Cold |

| Arizona | $1,900 | $158 | Wildfires |

| Arkansas | $3,500 | $292 | Severe Storms/Hail |

| California | $1,400 | $117 | Wildfires (High Variation) |

| Colorado | $3,100 | $258 | Wildfires/Hail |

| Connecticut | $1,600 | $133 | Coastal Storms |

| Delaware | $780 | $65 | Coastal Flooding |

| Florida | $6,000+ | $500+ | Hurricanes/Litigation |

| Georgia | $2,200 | $183 | Storms/Hurricanes |

| Illinois | $1,850 | $154 | Wind/Thunderstorms |

| Louisiana | $5,300 | $442 | Hurricanes |

| Massachusetts | $1,550 | $129 | Winter Storms |

| New York | $1,600 | $133 | Coastal Storms |

| Ohio | $1,300 | $108 | Wind/Hail |

| Texas | $4,100 | $342 | Hurricanes/Hail/Tornadoes |

| Wyoming | $1,700 | $142 | Wind/Wildfires |

Why Does Location Matter So Much?

When an actuary calculates your premium, they aren't just looking at your house; they are looking at your neighborhood, your city, and your state. Here is why geography is destiny in the insurance world:

1. Weather Patterns (Catastrophe Risk)

This is the single biggest driver of cost. If you live in "Tornado Alley" (parts of TX, OK, KS, NE), your home is statistically more likely to suffer a total loss than a home in Vermont. Insurers must collect enough premiums from everyone in that risk pool to pay for the massive payouts that occur after a major storm. Similarly, coastal states face hurricane risks, while western states face wildfire risks.

2. Construction & Labor Costs

Dwelling coverage is based on the cost to rebuild, not the market value. If a state has a shortage of construction workers or high material costs (often due to high demand after storms), rebuilding a home becomes more expensive. This drives up the coverage limits you need, and consequently, your premium.

3. Regulatory Environment

Insurance is regulated at the state level. Some states have laws that make it difficult for insurers to raise rates quickly or limit non-renewals. While this protects consumers in the short term, it can sometimes lead to insurers leaving the state entirely or becoming very selective, which reduces competition and drives up prices for remaining options.

Living in a High-Cost State? Here is What To Do

If you see your state at the top of the "most expensive" list, do not panic. You cannot move your house, but you can move the needle on your premium:

- check_circle Wind Mitigation: In states like FL and LA, a wind mitigation inspection that proves your roof is strapped down correctly can save you up to 40%.

- check_circle Shop Every 6 Months: In volatile markets, rates change fast. Loyalty rarely pays. Check competitors frequently.

- check_circle Consider the FAIRT Plan: As a last resort, most states offer a "Fair Access to Insurance Requirements" plan for high-risk homes that cannot get private coverage.

Conclusion

The disparity in home insurance costs across the USA is a stark reminder that where you live impacts your wallet in ways beyond just taxes and housing prices. While you can't control the weather or state regulations, understanding where your state stands gives you a baseline for negotiation. If you are paying significantly more than your state's average, it is a clear signal that it is time to shop around.

HomeInsuranceQuotes360 Team

Data Analysis Unit