Condo Insurance vs. Home Insurance: What’s the Difference?

Buying a condo is very different from buying a house, and insuring one is even more confusing. Who pays for the roof? What if my neighbor's pipe bursts? Do I own the drywall?

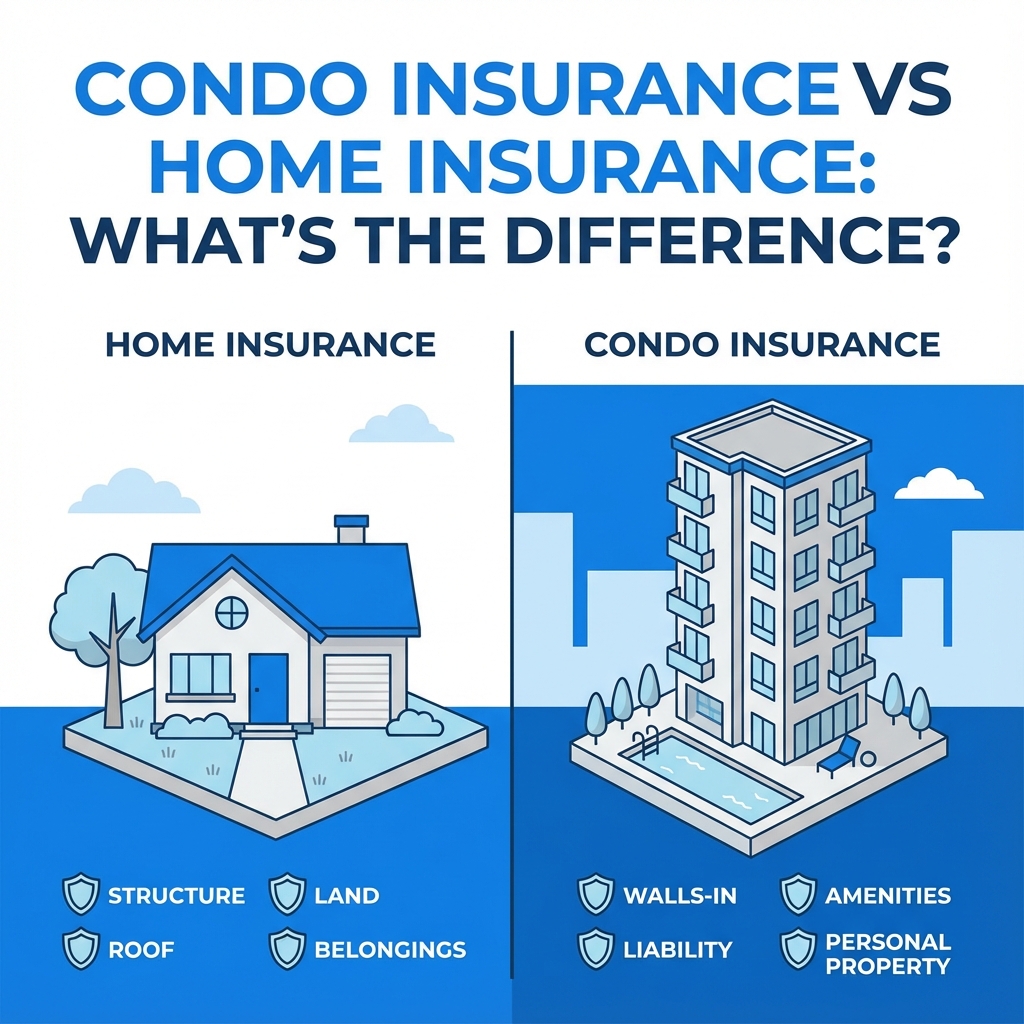

Let's break down the difference between the HO-3 (Homeowners) and HO-6 (Condo Unit Owners) policies.

The Big Difference: What You Own

Single Family Home

You own everything: the roof, the siding, the land, the trees, and the driveway.

You need: HO-3 Policy

Condo Unit

You only own the interior of your unit ("walls-in"). The Homeowners Association (HOA) owns the roof, hallways, elevators, and exterior walls.

You need: HO-6 Policy

HO-6 Coverage: The "Walls-In" Rule

Your biggest challenge is understanding where your responsibility starts and the HOA's ends. This is defined in your condo association's bylaws ("CC&Rs"). There are three common types:

1. Bare Walls Coverage

The HOA covers the drywall and framing. You are responsible for paint, flooring, cabinets, fixtures, and appliances.

2. All-In Coverage

The HOA covers the original fixtures (cabinets, floors) as they were built. You only need to insure your personal belongings and any upgrades you made (e.g., if you replaced the carpet with hardwood).

3. Single Entity

A hybrid where the HOA covers standard fixtures but not upgrades.

Pro Tip: Never guess. Bring your HOA bylaws to your insurance agent so they can read the insurance requirements section.

Loss Assessment: The Hidden Risk

This is unique to condos. Imagine a guest slips in the secure lobby (HOA property) and sues the HOA for $2 million. The HOA's liability policy only covers $1 million. The remaining $1 million is split among the 100 unit owners.

Suddenly, you get a bill for $10,000 payable in 30 days.

Loss Assessment Coverage pays this bill for you. It costs about $15 a year to add $50,000 of coverage. Do not skip this!

Condo vs. Home Cost Comparison

| Feature | House (HO-3) | Condo (HO-6) |

|---|---|---|

| Dwelling Coverage | $300,000 (Full Structure) | $60,000 (Interior Only) |

| Liability | $300,000 | $300,000 |

| Avg. Monthly Cost | $150 - $250 | $40 - $80 |

Conclusion

Condo insurance is cheaper but trickier than home insurance. The key is understanding your HOA's master policy so you don't double-insure or under-insure. And remember: Loss Assessment coverage is non-negotiable.

Frequently Asked Questions

What if my upstairs neighbor floods my unit? expand_more

HomeInsuranceQuotes360 Team

Condo Specialists